While your incredible, unique, surefire business idea will be sure to captivate investors, you won’t get very far in finding financial support unless you can also tell its financial story. That’s the purpose of your business financial plan—to show your potential funders what a good bet this is. You aren’t just a dreamer. You’re a doer. You’re business financial plan shows this.

“The goal is to show your lender that you are a reliable and resilient borrower to give them confidence in their decision,” Bill Phelan, CEO of PayNet, an Equifax Company, told Foundr.

Foundr understands that this part of getting your business off the ground can be intimidating. You might even be tempted to put it off or ignore it entirely, hoping a magical unicorn will notice how hard you’re working and how good your idea is and just pop up with a check.

Come on back to reality and let’s do this.

On the major plus side, this endeavor doesn’t only serve the people who are holding the cash you need. Creating the five elements of your business financial plan (income forecast, expense budget, cash flow snapshot, assets and liabilities disclosure, and break even analysis) serves you.

Writing your business financial plan forces you to take an honest look at what you’re about to attempt. You’ll have to think not just about today’s exciting idea, but the intricacies of how that idea will come to fruition in a nearby tomorrow.

Chances are high that you will spot any potential financial pitfalls as you create this plan, instead of crashing into them six months from now and watching all your work go down in flames.

This isn’t rocket science, it’s entrepreneurship. And you’re here for that—for all of that—right?

Then let’s get to it.

Financial plans typically include five elements:

The exact order and terminology may vary, but the information that should be included boils down to those five areas. Let’s walk through each one and you’ll see how simple this is.

Just write, “I’m going to make a million dollars in three weeks!”

Do not write that, or anything remotely resembling it. Yes, even if you just know that it is absolutely 100% true for your amazing idea.

The sales forecast is your opportunity to show a lender or investor that you are not a starry-eyed dilettante who will blow through their cash. This is your moment to be reasonable and mature. Feel free to drink a cup of tea (pinky raised) and speak in a lofty British accent while you write out the list of ways you will make money. Is it product sales? Advertising? Memberships?

Now, the time has come to validate your dreams with a warm, comforting coat of research-based estimates. Find a product or service that is similar to yours. Now find two more. Look at the sales of those products or services. Consider how they are each similar to or different than yours. What do you plan to do differently? How will your product or service cause a different reaction in the market?

Now assign sales figures to each item listed in your income source list, based on similar sales in your industry and your reflection on your idea’s potential compared to their reality. Keep in mind that your numbers here are not set in stone. They are your informed best estimate, and you will explain how you arrived at that estimate when you sit with a lender or investor discussing the plan you’re now writing.

For instance, let’s say you have designed a beautiful, one-of-a-kind fork. It provides all the services of the billions of existing forks on the planet—but it also records how many calories it forks into your mouth and reports those to the health app on your iPhone. (Also, it’s dishwasher safe!)

You could research sales of forks and sales of health gadgets, then use the information from that to form best guesses for how your new Fork Dork could sell.

Later, when you’re sitting with Mrs. Josephine Banker and telling her how you need a $2.3 million loan to create a prototype, you will be able to say, “Look at all the forks that sell every year already, Mrs. Banker. Obviously, forks are in major use. Now take a look at the billions that are spent on calorie counters and food trackers. See what a credible profit potential this holds?”

Insider word of advice: Once you’ve created your estimate, cut it by 20%.

Trust me on this.

That way, when you’re sitting with Mr. Igor Investor, you’ll be able to say, “To be conservative and reasonable, I lowered my projections by 20%.” He’s going to appreciate this display of reason and perhaps attach more credibility, not only to your entire financial business plan, but to your business idea as a whole.

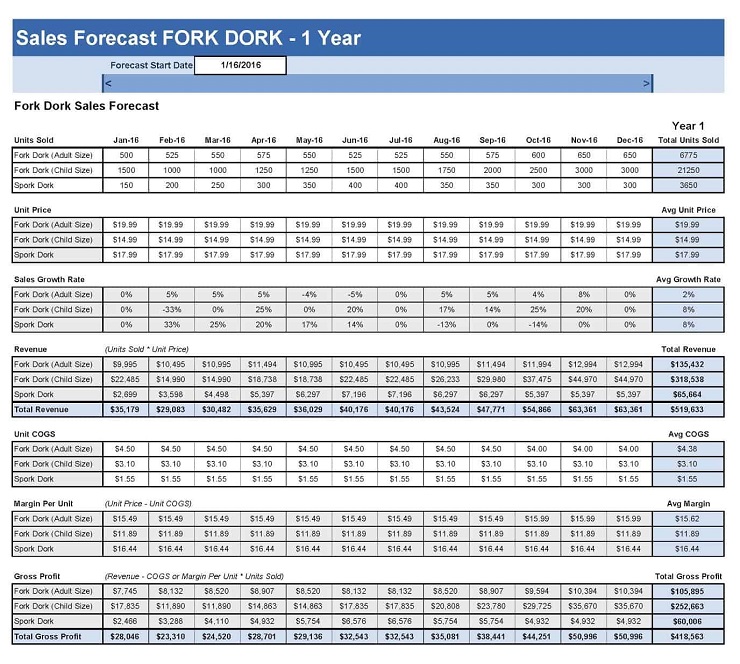

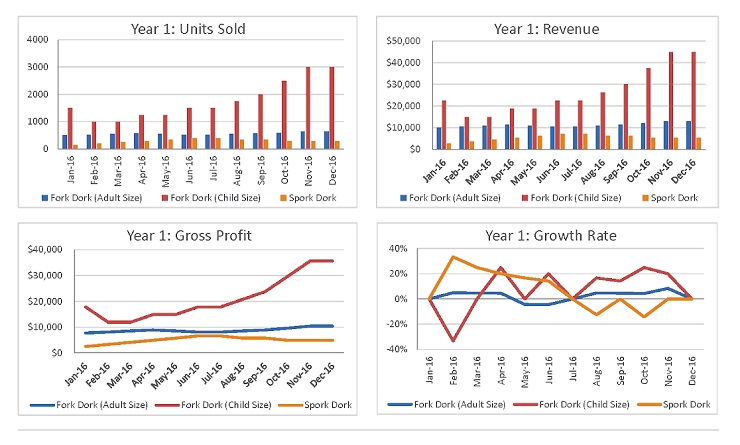

For those (like yours truly) who need a picture to explain number ideas, here’s an example of an sales forecast spreadsheet:

And here are some of the fun graphs that can be made with sales projections.

Download templates to create your own sales projection worksheets and charts at vertex42.com. Find the sales projection worksheets here.

Wouldn’t it be awesome if you had every dollar you needed before you needed it to build your business? What a fun fantasy.

And that’s all it will be, unless you put fantasy to paper. For your next business financial plan element, you’ll create an expense budget.

This is not the place to skimp or ignore. Here’s your opportunity to ask for everything you envision needing. You may not get it all, but you should absolutely include it all in the ask.

Remember that this is your opportunity to show how reasonable and logical you are. So, while you will include every potential expense you can imagine, you will also refrain from granting yourself a million dollar salary in the first six weeks with a half million dollar bonus two weeks later.

Be realistic. Learn to pronounce “boot strap” and “grow to go” (yes, you can do it in that British accent you perfected during the income forecasting).

In your expense budget, you’ll list salaries, contract worker fees, costs for equipment, research, office rent, supplies, software, subscriptions, travel, and more.

If this is your first go-round, a strong word of advice: Don’t forget to budget for legal (attorneys), accounting (bookkeepers and tax professionals), and tax payments (on payroll and sales). Some founders think they can skimp on these areas and squeak through with fingers crossed.

But if you want to build a business financial plan that reflects a mature, responsible approach (and not ruin yourself financially if this doesn’t work out), then you will include money for attorneys, accountants, and the government’s cut.

Also, include a line item for contingencies and miscellaneous. It should be 10-20% of your entire expense budget. So, if you tallied up everything you anticipate needing to spend for the year and it comes to $1 million, add $100,000-$200,000 in the “contingencies/miscellaneous” column.

It will feel excessive.

Mrs. Banker and Mr. Investor know it is not.

It is, instead, the line they know you will pull from when something unexpected inevitably happens, and that means you will most likely not be coming in their door with your hand out again.

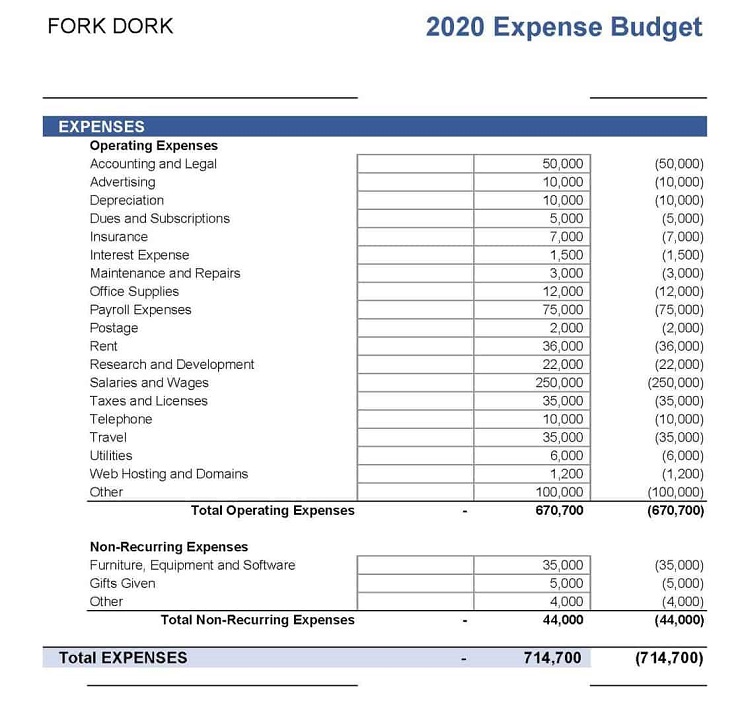

For my fellow visual learners, here’s an example of an expense budget:

Now that you’ve thought through where the money is coming from and where it’s going, you can create a Cash Flow Snapshot. This document gives you an idea of how much money you’ll have on hand for operations on any given day. It also lets your lender or investor see why you need operational money to get (or keep) going.

At first, the Cash Flow Snapshot can seem redundant. If 1,000 Fork Dorks are projected to sell in August for $40 each, then August income is $40,000, right?

Well, who bought the Fork Dorks? (There’s another business idea: a band called “Who Bought the Fork Dorks?”) If wholesalers bought them to re-sell in stores, then they might not be paying you for your product for 30, 60, or 90 days. So, $40,000 of product can go out in August, but it could be November before that $40,000 comes in as income. This is accrual accounting and something you can talk about with the accountant you intend to hire because you are a serious entrepreneur. By using accrual accounting to create your Cash Flow Snapshot, you’ll see that, if there is no other source of income than that $40,000 sale in August, the busy workers in the factory making Fork Dorks might well walk off the job.

You’d wind up Fork Dork-less!

Also, you’d be back in the banker or investor’s office with your hand out and a sheepish expression, explaining how you really, really are a smart, serious, trustworthy entrepreneur but you didn’t take into account something as simple as the gap between sale and payment.

Aren’t Cash Flow Snapshots awesome?

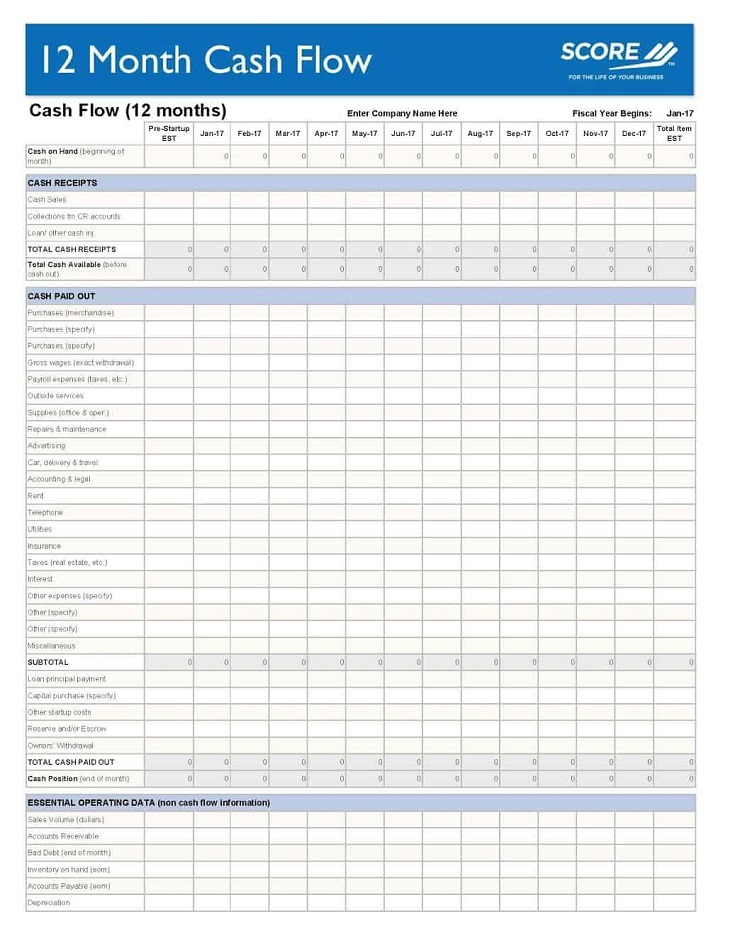

Visual learners, here’s your example of a blank Cash Flow Snapshot (download a template from SCORE here):

Okay, so we have a sheet that shows where the money is coming from, another one that shows where the money is being spent, and another that shows the ebb and flow of all that in monthly time. Lovely!

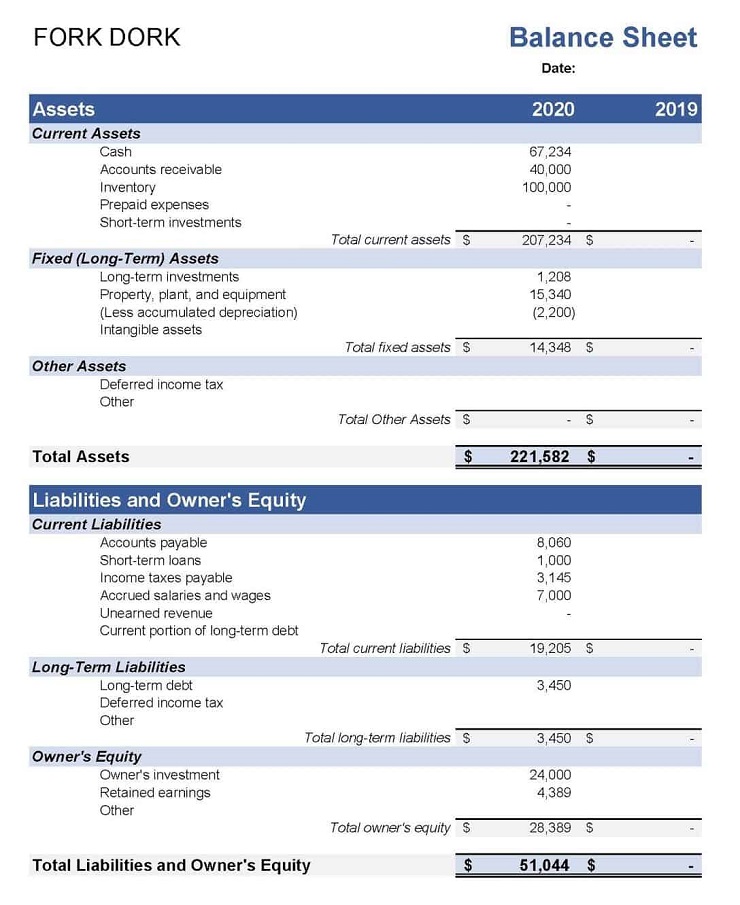

Now you’ll incorporate in whatever Mrs. Banker, Mr. Investor, and you have put into the business, as well as other elements, to create your Assets and Liabilities Sheet.

Assets include the money you have in the bank (both pennies!), the money that’s coming in (that $40,000 in November), the value of what you could sell but haven’t yet ($100,000 worth of Fork Dorks sitting on your warehouse shelves), Mr. Igor’s investments, any other investments (don’t group short-term and long-term investments into one line), any real estate or vehicles the company owns, any equipment—basically anything the company owns that could be sold for money.

Liabilities include everything the company owes. Imagine the company goes belly up. Now think about who would be owed money. Mrs. Banker’s loan (and interest that would be due). Payroll and taxes for your employees. Contracted worker fees. Other contracted fees (e.g. office rent for the remainder of the lease). List all of these in the liabilities section.

To figure out the net worth of your company, subtract your liabilities from your assets. For instance, if you owe $100,000 (liabilities) and you have $200,000 in assets, then your company’s net worth is $100,000. This is also called the owner’s equity because it’s the value of what the owners own by being owners of this business.

The Assets and Liabilities Sheet shows how the net worth of your business/owner’s equity changes from month to month or year to year as you pay off the liabilities and accrue assets.

Resist the urge to rub your hands together and giggle as you see the number head into a positive range and grow.

Well, go ahead, nobody’s watching. But only for a second.

Visual learners, here’s your example of an Assets and Liabilities Sheet (download a template to create yours from Vertex42 here):

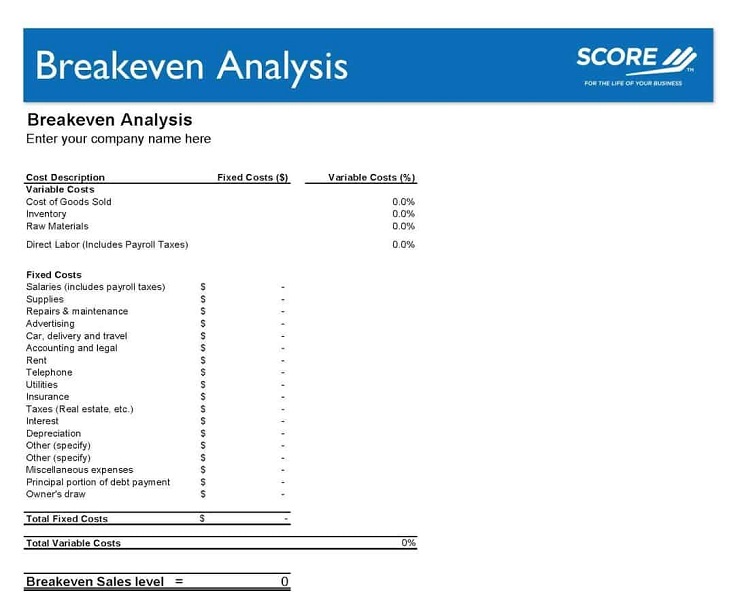

At last, you have reached the Final Frontier. Okay, not really. You’ve just come to the final element of writing a business financial plan: the Break Even Analysis.

This document is exactly what it sounds like, a reflection of when your company is going into the black and not going back. At what point do the numbers reflect that your company is making more than it’s spending? Mr. Investor is particularly interested in this part because it shows him when and how his gamble might pay off.

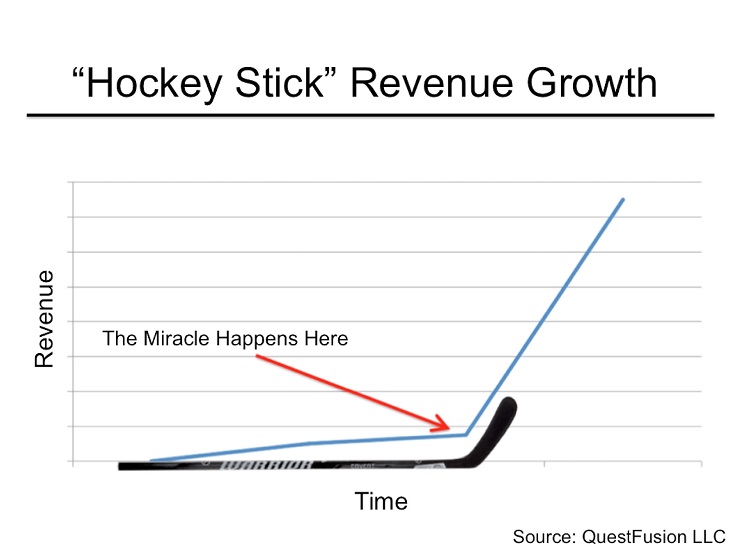

Remember how you absolutely, 100% are not going to show your sales hitting $1 million in three weeks? (If you’ve already forgotten that part of this article, then you might need to pause here and go Google “ginkgo biloba.”) A big reason for that is to avoid a “hockey stick” in your break even analysis.

They look like this:

Now, before a bunch of pucks get thrown at the Foundr offices, let’s be clear that this is not a bias against hockey. No, this is a bias against unrealistic expectations and projections (aka googly-eyed entrepreneurs). Put your most posh British accent back on and tell yourself, “I must be reasonable.”

Now create a spreadsheet that shows when your income moves beyond your expenses and stays there.

Here’s what one looks like (download yours from SCORE here):

You did it! You made it to the end of an article that had nothing to do with your creative product or service and everything to do with math, finance, accounting, and reasonable entrepreneurial endeavors. You now know how to create a business financial plan.

Or, you’re soon going to be.

But not of Fork Dork, Inc.

Any questions? Feel free to blast them in the comments below!

Rebeca Seitz is a best-selling writer and producer, and the founding CEO of 1C Productions, Inc. She recently raised over $3M for a single business venture and helped create, distribute, and promote products with sales of over $34M. Her books are published by HarperCollins and B&H Group and her last screenplay was produced with Out of Order Studios and written with Disney veteran Bob Burris. She has appeared on NPR, CNN, Huffington Post Live, and more regarding the responsible use of mass media.

Bootstrapping vs. External Funding: What’s Right For You?

How Much To Unapologetically Charge For Public Speaking

How to Get Sponsored: From 0 to $50,000 in 4 Weeks

How To Develop a Million-Dollar Pitch Deck For Potential Investors

Business Not Making Money? Here’s the Reason(s) Why

What Is ROI? And How Can You Calculate It like a Pro?

Profit and Loss Statement: What Is It and Why Your Business Needs One

How Much Do Consultants Make? Get Ready to Consult.

Business Startup Funding: A Beginner’s Guide

These Founders Bought Back Their Business: Chris Savage and Brendan Schwartz of Wistia

Annual Recurring Revenue: Calculate Your Subscription Revenue

Revenue vs Profit: What’s the Difference and Why it Matters

How to Build Business Credit Fast: Everything You Need to Know

Series Funding for Startups: Terms and Jargon Explained

16 Financial Concepts Every Entrepreneur Needs to Know